Ask any entrepreneur, and they’ll tell you strategy and planning are essential when it comes to running a business. One of the first things you need to plan for is your business start up costs.

In this article, we’ll walk you through how to estimate costs in theory and practice with a real-world example. We’ll also identify what the IRS officially regards as startup costs, so you can strategically time your expenses to maximize tax efficiency.

Launching a business can be challenging, but it’s a lot easier if you have a financial expert in your corner from day one. Our accounting services for small business can help you get started on the right foot.

Table of Contents

Before You Start: How Much Do You Need to Save?

The best way to estimate start up costs is to make a thorough list of every possible expense and seek quotes from relevant parties. (We’ve got a list below to help you get started.)

Once you’ve gathered estimates for one-time and recurring expenses, do the math and ensure you have access to six months of operating expenses available before you start. This will give you the financial runway you need to get your business off the ground.

Having this sum in cash is the least risky way to start, but in most cases, entrepreneurs also tap a combination of private investments, bank loans, and business credit cards.

If you need help securing startup funding, read our guide to SBA loan applications or contact an indinero small business expert today.

Our List of Common Start Up Costs

If this is your first time opening a new business, you may be unsure what start up costs you need to plan for. We’ve compiled this list, covering many common expenses and their average cost. However, your business is unique, so some of these expenses may not be applicable, or you may need to add others. Remember: You can get more accurate estimates by researching online and asking for quotes.

Incorporation Fees

Most states require a nominal fee to incorporate your business. This will vary depending on where you are setting up your business, but on average, you can expect to pay about $150 to register.

For more guidance on incorporating your business, check out our guide on choosing a limited liability corporation (LLC) vs sole proprietorship.

Office Space

Traditional office space can cost between $8-$23 per square foot, per month, while a coworking space costs between $250 and $500 per individual per month. Once again, these figures highly depend on where and how much space you want to rent out. Some businesses may be remote, so the office space cost would be much lower or non-existent.

Marketing

An established B2B business might spend 10% of annual revenue on marketing, while a B2C business may spend 5%. A 2023 Delloite survey of over 300 chief marketing officers revealed their average marketing spend to be ~9% of revenue.

For a specific reference, a survey of 1,500 Canadian small businesses found their average annual marketing spend to be $30,000.

Website

Forbes reports that the average small business website (up to 16 pages) could cost between $2,000-$9,000. Your expenses will depend largely on whether you or someone on your team plans to build the site or if you expect to hire a professional developer to get it live.

Utilities

According to the Building Owners and Managers Association, the average cost of commercial building utilities is ~$2 per square foot. If you plan on having a physical office space for you and your staff, make sure you are considering utilities like these.

New Technology or Machinery

Depending on what kind of business you’re starting, you may need to purchase new hardware or machinery to get your operation off the ground. Costs can vary widely depending on what you need. If you’re only looking to purchase a few new laptops or some online software, this start up cost might only be a few thousand dollars; for more expensive machinery, this expense can be much higher.

Consultants

According to Forbes, standard startup consultancy fees run between $75 and $400 an hour. Consider whether you plan to hire experts to help you get your business up and running, and find a few average prices for the types of consultants you’re looking for to estimate this cost.

Start Up Costs Example

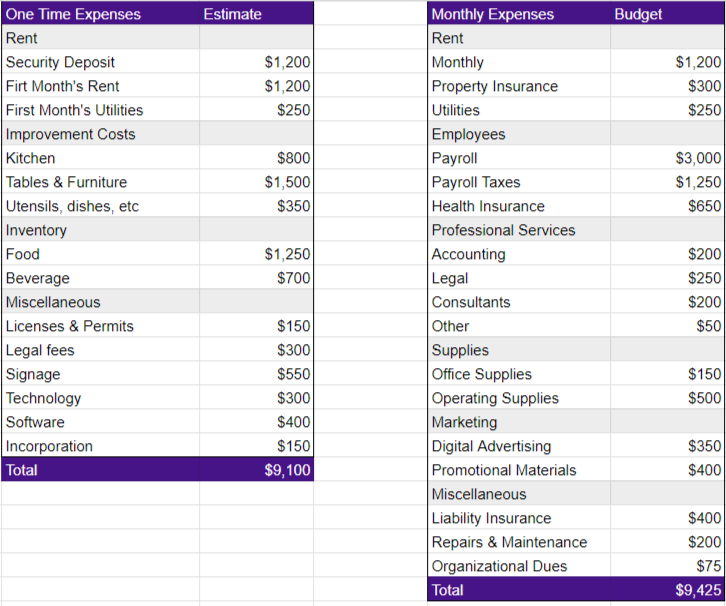

To further illustrate what your startup costs for business might look like, consider the fictional case of Rita’s doughnut shop. We pulled these cost estimates from the Small Business Administration (SBA).

In Rita’s case, if she followed our recommendation of having six months of operating expenses available, she would need $65,000 to shart her shop.

Rita’s Doughnut Shop

Start Up Costs Tax Treatment: How to Maximize Your Tax Expenses

Now that you’ve estimated your startup costs, it’s time to use them to save money on your upcoming tax bill. Here’s what to consider:

What Time Period Is Your Business In?

The IRS divides your business into two time periods: startup mode and the active trade or business period. This distinction is important, as deductions come more easily during the active period.

A business becomes an active trade or business when it’s ready to start selling its core product or services. Before that point, it was in startup mode.

Startup mode often ends when the first sale is made, but not always. Sometimes, miscellaneous income is earned but the business continues to be in startup mode. Other times, even though it hasn’t made a sale yet, a business is no longer a startup in the eyes of the IRS because it’s ready to fulfill its primary business purpose.

In startup mode, deductions are limited to $5,000 for capital expenditures and $5,000 for organizational costs. All other deductions are put on hold until the business becomes active in the eyes of the IRS. If your total costs exceed $50,000, the cap grows smaller: The $5,000 maximum is reduced by every dollar over $50,000 you spend during the startup period.

From here, your startup costs are amortized evenly over the next fifteen years. If the business shuts down, any remaining un-deducted startup costs are fully deductible on the final year’s tax return. Any loss in excess of profit is eligible for a net operating loss carryforward.

Should You Spend During the Start Up or Active Period?

Let’s say your business incurs $150,000 in startup costs. When it becomes active, you’ll start deducting these costs at $10,000 per year. These deductions are locked and are released over fifteen years.

However, is it mandatory to incur all of those expenses before entering the active phase of your business? No. By deferring what you can until after the startup phase, you are eligible for those deductions in full the year they occurred.

Qualifying Start Up Costs

The IRS has a simple definition of qualifying business start up costs. It comes down to two factors, and any expense that meets both criteria counts as a start up cost:

- It’s a cost that would be considered “ordinary and necessary” for operating a business during the active period. For future reference, this is the same definition that qualifies expenses for small business tax deductions.

- It’s a cost a business pays or incurs before the day their active trade or business begins.

Nonqualifying Start Up Costs

The IRS prohibits deductible interest, taxes, and research and development (R&D) expenditures (defined as research and experimental costs normally occurring in a laboratory or product testing environment). Software development as well as attorney fees for obtaining a patent are also considered R&D expenses, and therefore don’t qualify for deductions.

Can You Deduct Start Up Costs With No Income?

Yes, you can deduct startup costs even if your business has no income in the initial stages. The IRS allows entrepreneurs to deduct qualifying startup costs, regardless of whether the business generates revenue in its early days.

How to Claim the Start Up Tax Deduction

Simply deduct the startup or organizational costs on your income tax return for the year the active trade or business begins.

If you file on time but forget to claim the deduction, you may do so by filing an amended return within six months of the due date of the return (including extensions).

Conclusion

Forecasting business start up costs is challenging, especially if you’re a first-time business owner. While there’s no substitute for real-life quotes and cost estimates, we hope our article provided a reasonable place to begin your planning process.

Remember to secure at least six months of operating expenses before starting your business and, to save on taxes, delay any expenses you can until after the startup phase.

Before you go, consider taking the time to read our article on how to keep track of business expenses. Doing so will save you headaches come tax time.

Best of luck in your journey to entrepreneurial success. When you reach a stage where you need accounting help, we are always here to provide affordable accounting services for small businesses.

{kind=link}